Owning a home is more than just having a roof over your head—it’s about having your own space, a place you can truly call your own. For most people, especially in the middle class, buying a house isn’t possible without taking a home loan. But once you decide to borrow, a common question arises: If I take a loan of ₹18 lakh, what will my monthly EMI look like? Let’s break it down in a simple and easy way, without any confusing banking jargon.

What Exactly Is a Home Loan?

Think of a home loan as financial help from a bank to buy your house. You borrow a certain amount, called the principal, and pay it back in small monthly installments called EMIs (Equated Monthly Installments). These EMIs include part of the principal amount plus interest charged by the bank. Since home loans are secured by the property itself, banks usually offer lower interest rates compared to personal loans. In India, the interest rates generally range from about 8.5% to 9.5% annually. You can choose to repay the loan anywhere between 10 to 30 years. Keep in mind, a longer tenure means smaller monthly EMIs but higher total interest paid over time, while a shorter tenure means larger EMIs but less interest overall. It’s all about balancing your comfort with savings.

How Much Will the EMI Be for ₹18 Lakh?

Let’s look at some examples to understand how EMIs change depending on loan tenure and interest rates:

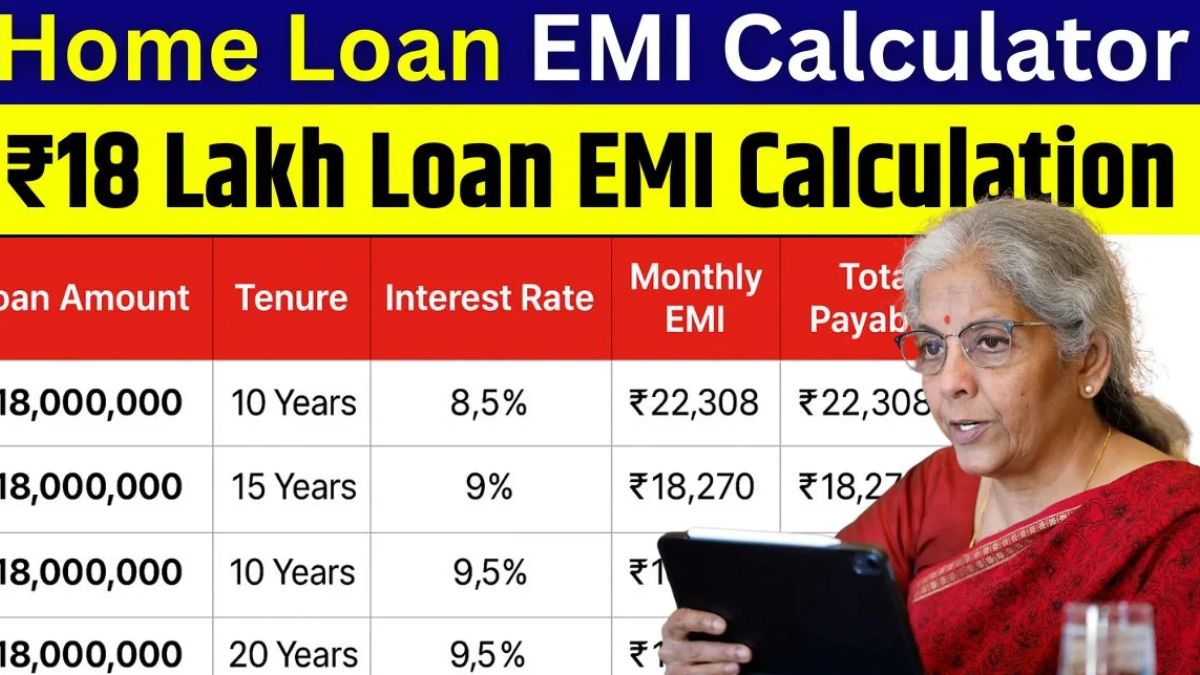

| Loan Amount | Tenure | Interest Rate | Monthly EMI | Total Interest Paid | Total Amount Paid |

|---|---|---|---|---|---|

| ₹18,00,000 | 10 Years | 8.5% | ₹22,308 | ₹9,67,000 | ₹27,67,000 |

| ₹18,00,000 | 15 Years | 9% | ₹18,270 | ₹14,88,600 | ₹32,88,600 |

| ₹18,00,000 | 20 Years | 9.5% | ₹16,737 | ₹22,56,880 | ₹40,56,880 |

As you can see, opting for a 10-year loan means a higher EMI of about ₹22,300 but lower interest cost overall. Stretching the loan to 20 years reduces your monthly EMI to around ₹16,700, which might be easier on your monthly budget but ends up costing much more in interest.

Why Your CIBIL Score and Income Matter

Banks want to lend money to people they can trust. If you have a good credit score (above 750), you’re more likely to get a lower interest rate, which means cheaper EMIs. A steady income also helps convince banks that you can repay on time. On the other hand, a low credit score can push banks to charge higher interest rates since it’s riskier for them.

Home Loan: Not a Burden, But an Investment

Many people see loans as stressful, but a home loan is actually an investment in your future. Instead of paying rent to someone else, your EMI goes toward owning your own home. Plus, you can save money through tax benefits under sections 80C and 24(b) of the Income Tax Act. These deductions on both principal and interest reduce your taxable income, giving you real savings.

For an ₹18 lakh home loan, expect your monthly EMI to be somewhere between ₹16,000 and ₹22,000, depending on how long you choose to repay and the interest rate offered. Remember, this is a step toward owning your dream home, not just a financial burden. The key is to borrow wisely, keep your repayments on track, and gradually build your way to homeownership.